Economic growth is the worst

A quick summary

Economists push the need for more and more economic growth

But economic growth has very serious negative consequences

But also: economic growth is super important. It boosts people’s living standards and creates the resources to fund a range of economic initiatives

The challenge is how to grow in a way that mitigates some of the negative impacts

Don’t be fooled

“Economic growth is terrific.”

You hear this from your teacher or an economist or maybe even a politician.

But I implore you: be skeptical of this claim. Economic growth is terrible*.

I’ve got four reasons why economic growth sucks. Or, in a more articulate way, there are four negative consequences of economic growth.

(*Please read all the way to the end.)

Economic growth is terrible because it results in higher prices

Let’s say economic growth is rising in an economy. So aggregate demand is rising…however, firms may not have enough time to increase production to match this rise in demand.

Look at it from this perspective. As the economy grows, consumers’ incomes rise. This means they can afford more goods and services. However, there is limited stock of goods and services.

“In fact, consumers use their extra income to ‘bid up’ the prices of limited goods and services, which then results in higher prices. I like to think about extra money ‘chasing’ the same amount of goods and services.”

So we would say that the rise in aggregate demand is outstripping aggregate supply (because firms haven’t had time to produce more goods and services). This leads to demand-pull inflation.

[Just remember: aggregate demand affects economic growth in the short term, while aggregate supply affects growth in the longer term.]

But we may also see cost-push inflation. This is because higher economic growth leads to greater demand for the inputs of production, which will lead to higher costs for businesses.

Think about it this way: economic growth leads to greater demand for labour, which will result in lower unemployment. As firms need more and more workers, they will need to pay higher wages to poach them from other firms (because unemployment is so low). This leads to higher inputs costs (wages) which will result in firms pushing up the prices of goods and services (cost-push inflation).

Also, during a period of economic growth, many firms will demand more inputs to meet the higher demand for goods and services. As a result, the prices of inputs like raw materials will also rise and this will further lead to cost-push inflation.

Learn more about cost-push inflation

Economic growth is terrible because it results in higher prices and then higher interest rates

As we’ve seen in the previous section, higher economic growth generally leads to rising inflation.

If inflation is rising in Australia, the central bank will act. The Reserve Bank will raise the cash rate, the official level of interest rates, to indirectly increase interest rates across the economy and slow inflation.

What’s the issue with the higher rates?

The RBA will act.

Australia’s central bank will adjust the cash rate if inflationary pressures are rising.

Higher interest rates will result in less investment. This is because higher rates mean higher interest repayments for borrowers.

Higher interest rates could also result in a higher exchange rate. This is because more foreign investors could be motivated to save their money in Australia as the returns could be higher. A higher exchange rate could make Australian exports less competitive.

Economic growth is terrible because it results in environmental degradation (and therefore lower living standards)

Economic growth is still highly dependent on the use of fossil fuels. In order to increase output, we need to use non-renewable resources, such as oil and minerals, which reduces the ability of future generations to harness these resources.

The more economic growth, the more pollution.

In addition, the use of fossil fuels leads to higher pollution. This leads to environmental degradation (which may not be fixable) and potentially lower living standards. Think about how pollution could result in poorer air or water quality. This has negative implications for future generations.

Economic growth is terrible because it can worsen income and wealth inequality

This is a trickier point. One view is that economic growth will reduce income inequality as it results in higher wages for lower-income earners. Or that it leads to the unemployed gaining jobs which then leads to them having higher wages. And overall, income inequality is reduced.

There’s another view to consider.

The wealthier people in society own more assets, including shares, homes and investment properties. So if the economy grows and asset values rise, this would deliver greater benefits to those who are already wealthy. They would receive greater dividends, rent and other incomes flows from their assets. According to this view, as economic growth rises, income and wealth inequality could rise.

*But we need economic growth

Yes, economic growth has negative consequences. Quite serious negative consequences in some cases. But we need economic growth.

This blog post has a deliberately sarcastic tone. Don’t start writing essays where you make the case for GDP growth of 0%. This will be unhelpful for your marks.

You see, economic growth delivers so many benefits to a country and its population, including rising living standards and higher wages.

The issue here is how we pursue economic and growth and what do we do with the benefits of economic growth.

For example, could countries try to grow more sustainably, with less of a reliance on fossil fuels? And could countries direct some of their benefits from economic growth to addressing some of the negative consequences of growth?

We can’t choose not to grow. But we can talk about how economies should choose how they grow.

How do movements in the TERMS OF TRADE affect the Australian economy?

Quick summary

Australia’s Terms of Trade is the ratio between export prices and import prices for the economy. It is a ratio that involves prices, NOT volumes

An improvement in the Terms of Trade means export prices are rising faster than import prices. This is likely to lead to higher economic growth and rising living standards

An improvement in the Terms of Trade means import prices are rising faster than export prices. This could accelerate AND slow economic growth (confusing!) but would likely lower living standards

Thanks for the question Emily!

Big shout out to Emily S for her great comment below.

[VCE is the final high school exam for students in Victoria.]

I read Emily’s question and it set my brain on fire. What a great question. Time for a comprehensive answer.

I’m going to go beyond Emily’s scope and discuss the impact of a favourable and unfavourable movement in the Terms of Trade. I hope she doesn’t mind.

What is the Terms of Trade?

It’s worth starting with a definition: the Terms of Trade (TOT) is the ratio of export prices to import prices.

The terms of trade index = (export price index/import price index)*100

The TOT is a measure of the prices of exports and imports. It does NOT measure volumes.

Think about it this way:

Export prices represent income for an economy. If Australia sells exports to China, the goods or services go to China BUT the revenue arrives in Australia. Exports are an injection for the Australian economy.

Import prices represent a cost for an economy. If Australia buys imports from China, the goods or services arrive in Australia BUT income leaves Australia and arrives in China. In this way, imports are a leakage for the Australian economy.

What does the Terms of Trade show?

For an economy, exports represent revenue and imports represent costs.

If exports prices rise relative to import prices (so export prices rise faster than import prices), then a country can afford to buy more imports with the same volume of exports.

If import prices rise relative to export prices (so import prices rise faster than export prices), then a country can afford to buy less imports with the same volume of exports.

Here’s a way to think about it. Export prices represent the amount of income Australia earns. If Australia earns more (export prices rise in relative terms), it can buy more stuff. And stuff = imports.

If Australia earns less (export prices fall in relative terms), it can buy less stuff. And stuff = imports.

Still confused about what the Terms of Trade means?

Check out my video setting out the concept.

What happens to the Australian economy when the Terms of Trade improves?

This is what’s known as a favourable movement in the TOT.

When the TOT improves, this means export prices are rising faster than import prices.

If export prices are higher, this means that Australia is earning more revenue from the sale of exports. This is because for every export sold, Australia receives more revenue (NOT PROFIT).

When Australia’s TOT improves, this is usually due to higher prices for Australia’s natural resources and/or rural commodity exports. These rising prices send a signal to investors that demand for some of Australia’s exports is growing and it may be a good time to invest in the natural resource and rural sectors. If they invest now, they can hopefully earn a higher return as the growth continues.

So, there are a number of consequences from this change in the TOT:

There will be greater investment in Australia’s export sectors. This will increase capital inflows (foreign direct investment and portfolio investment) and lead to greater income outflows (as recorded in the Balance of Payments)

There will be greater demand for workers in the export sectors. Rising prices are due to higher demand; higher demand means that local firms may need extra workers to meet the rising demand. The extra foreign investment means they are extra resources to pay for more workers. As a result, employment could grow in the export sector.

In addition, a favourable movement in the TOT means that Australians can now buy more imports with the same volume of exports. This means Australians can afford more goods and services. As a result, living standards will improve.

Let’s go back to Emily’s question (not her real one but my expanded one)

How would a favourable movement in the TOT affect strong and sustainable economic growth and living standards?

Economic growth will rise.

This is because export volumes are likely to be rising. Rising prices are a signal of higher demand. Exports are a component of aggregate demand. So: higher export sales, higher economic growth.

This is also because investment is likely to be rising. This is because more people will invest in Australia’s export industries when prices are rising. Investment is a component of aggregate demand. So: higher investment, higher economic growth.

And then living standards will be higher. This is because Australians can buy more imports (good and services) with the same volume of exports. This, in turn, is because exports command higher prices.

What happens to the Australian economy when the Terms of Trade worsens?

This is what’s known as an unfavourable movement in the TOT.

It is also referred to as a deterioration in the TOT.

When the TOT worsens, this means export prices are rising faster than import prices.

If export prices are relatively lower, this means that Australia is earning less revenue from the sale of exports. This is because for every export sold, Australia receives less revenue (NOT PROFIT).

When Australia’s TOT deteriorates, Australians can buy fewer imports with the same volume of exports. This means that Australians can afford fewer imported goods and services. Therefore, living standards will worsen.

If Australia’s export prices are relatively lower, then there could be less interest in investing in Australia’s export sectors. This could reduce capital inflows (FDI and portfolio) and then reduce the size of income outflows.

Here’s a tricky part. If Australia’s TOT worsens, then Australia’s exports command relatively lower prices. This could actually make them more competitive. As a result, we could see greater demand for Australia’s exports. This would lead to greater sales of export volumes, which would boost aggregate demand and economic growth.

Basically: if the TOT worsens, then Australia’s exports are relatively cheaper. This means Australia could sell more and economic growth could improve.

Let’s go back to Emily’s actual question

How would an unfavourable movement in the TOT affect strong and sustainable economic growth and living standards?

Living standards would be lower. This is because Australians could afford fewer imported goods and services. Why? Because the same volume of exports can now purchase a smaller amount of imports.

For economic growth, there are some competing events.

Export volumes could be falling. This is because fallings prices are a signal of lower demand. Exports are a component of aggregate demand. So: lower export sales, lower economic growth.

Then investment could be falling. This is because less people will invest in Australia’s export industries when prices are falling. Investment is a component of aggregate demand. So: higher investment, higher economic growth.

But! If exports are relatively cheaper, then more people may wish to buy them. These exports are now more internationally competitive. This could increase export volumes and increase economic growth (over time).

Which factor would have a bigger impact? It would depend. But if you discuss both possibilities (higher and lower growth), this shows the marker you understand the complexity of this economic theory.

The connection between elasticity and the Terms of Trade

Elasticity of demand relates to the sensitivity of quantity demanded to a change in price.

If export prices rise, we would usually expect the demand for export prices to fall. This would be true for elastic goods. A small rise in price would lead to a large fall in quantity demanded.

But what happens if quantity demanded is inelastic? This means that a moderate rise in price may only lead to a small fall in quantity demanded.

We can consider Australia’s commodity exports as relatively inelastic. This is because they are high quality, highly sought after and available in large quantities. So even if the price of these exports rise, countries such as China will still want to buy large amounts of exports.

So if the exports are relatively inelastic, even if the TOT improves, other countries will still purchase large volumes of Australia’s exports and economic growth will rise.

Ask your questions!

Thanks again to Emily for the question. Hopefully this answer helps. Send me your questions!

Now take a look at recent developments in Australia’s Terms of Trade in the video below.

Does Australia have a current account surplus? (Yes -- and it's kind of a big deal)

The quick version:

Australia has a current account surplus (CAS)

This is the first time Australia has recorded a CAS since the late 1970s

Australia’s CAS is caused by its Balance on Goods and Services surplus. The Net Primary Income balance is still in deficit.

Australia has a current account surplus. This is important

When I studied Economics at high school we never talked about a current account surplus (the CAS). Australia simply didn’t record a CAS. Instead, Australia was known for its current account deficits (CAD).

Things have changed in 2022. Australia has had a CAS for a period of time and it’s an economic statistic that signals some important things about the Australian economy.

Let’s rewind a little.

My HSC Economics exam and writing about a current account deficit

When I sat my HSC Economics exam, we only ever wrote about Australia having a current account deficit. We NEVER talked about current account surpluses.

Have a look at this stimulus for one of the essay questions.

Source: NESA

You can see that the current account balance for 1997/98 was a deficit for $23 billion. Let’s fast forward to now.

In the September quarter of 2021, Australia recorded a CAS of nearly $22 billion.

This CAS shrank to around $13 billion in the December quarter. But Australia still has a current account surplus.

On a personal note, I never thought Australia would have a CAS. Why would I? Have a look at this graph below. For my lifetime (up until now), Australia has had a persistent CAD.

The numbers on the right hand side of the graph represent the size of the current account balance as a percentage of GDP. So the larger the % of GDP, the larger the size of the CAD. You can see that in the mid-2000s the CAD was over 7% of GDP – a very large amount.

Why does Australia have a current account surplus in 2022?

The key drivers of Australia’s CA balance are:

The Balance on Goods and Services (BoGS)

The Net Primary Income (NPY) balance

As the value of BoGS and NPY change, so does the balance on the current account. Typically, Australia’s BoGS fluctuates considerably – due to the frequent changes in the prices and volumes of our exports. For example, the price of iron ore rarely stays the same. It’s not like manufactured goods that have relatively consistent prices. An iPhone’s price doesn’t fluctuate from day to day.

Australia has a persistent NPY deficit. This hasn’t changed.

So why has the CA has moved into surplus? Because of Australia’s BoGS surplus.

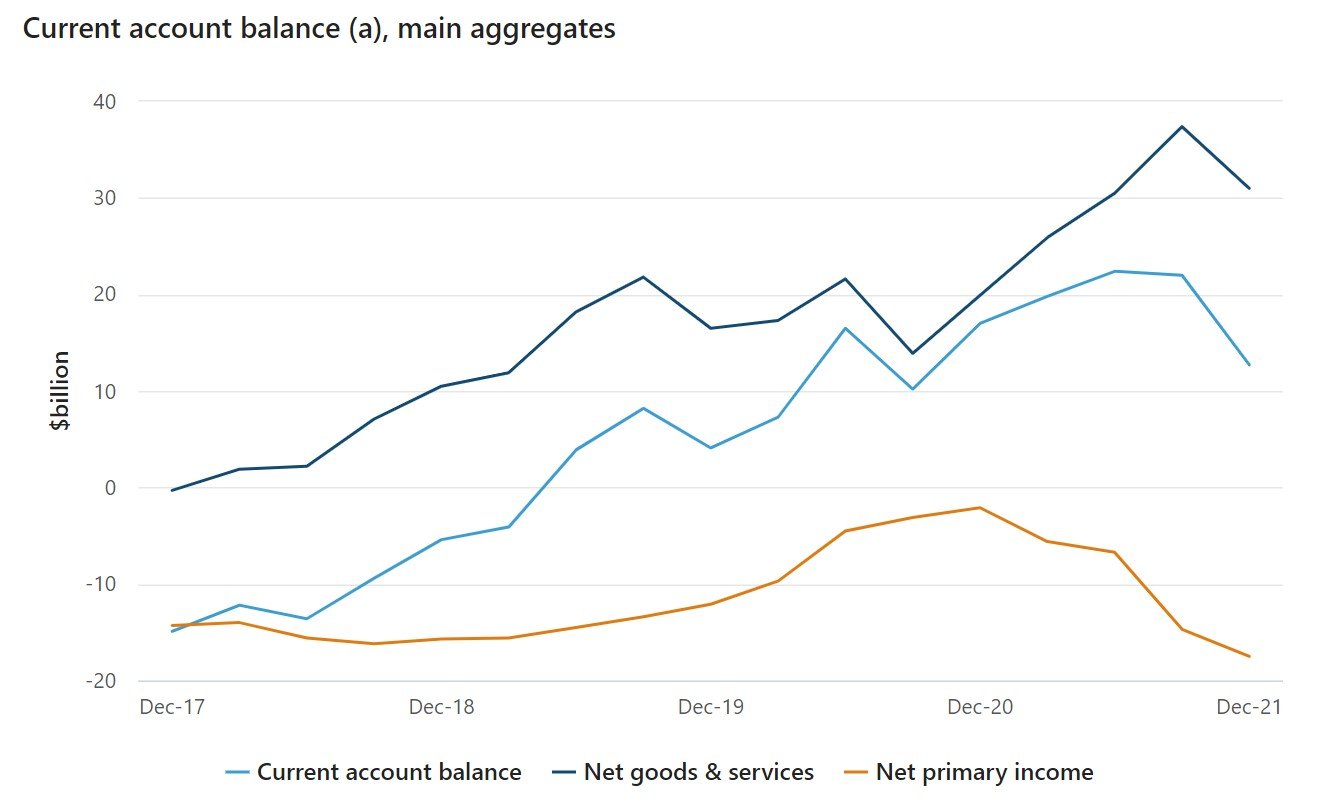

Have a look at this graph.

Source: Australian Bureau of Statistics

You can see that BoGS – the dark blue line – is leading the CA balance higher into surplus.

NPY is actually getting larger – the deficit is growing. This is pushing the CA balance the other way — so reducing the size of the surplus.

So the driver of the current CA surplus is the BoGS surplus. You can also call BoGS the trade balance or net exports.

Australia’s BoGS surplus is caused by an increase in Australia’s export sales (particularly of natural resources) and a slowdown in import spending (due to the impact of the pandemic).

What are the consequences of Australia’s CAS?

Here are some of the consequences of Australia’s CAS.

As Australia is selling more exports, there is greater demand for labour/resources into the export sector. This is to meet the growing demand for overseas markets.

Australia may also require greater investment in the mining sector to help increase the volume of natural resources that can be obtained and sold overseas. This could increase capital inflows in the form of loans from overseas. This, in turn, will increase income outflows and then increase the value of the NPY deficit.

In addition, as exports will be growing, they will contribute more to Australia’s aggregate demand. This is because AD = C+I+G+(X-M). So, as exports volumes rise, they will positively influence net exports (X-M), which will add positively to AD and the nation’s economic growth.

Not a lot of people are talking about the CAS. But they should be. It’s a very important statistic with important consequences for the Australian economy.

Want more on why Australia has a current account surplus?

I also have this video that looks at the drivers of a CAS (see below). It could be very helpful in trying to grasp this potentially tricky concept. A concept I never thought I’d see in my life.

Your favourite businesses are raising prices. Here's why

The quick version:

Cost-push inflation is when rising input costs lead businesses to raise retail prices

Rising input prices include higher wages, energy and rent costs (these higher costs push up retail prices)

Cost-push inflation is happening in Australia in 2022. According to the National Australia Bank, business purchase costs are at record levels. This is leading to higher inflation in the Australian economy.

Cost-push inflation is rising in Australia.

What is cost-push inflation?

Cost-push inflation is a cause of inflation. It occurs when higher input costs for businesses PUSH UP prices across the economy.

Basically firms face higher input costs and, rather than absorb these costs and reduce profits, they pass on higher costs to consumers.

The end result: consumers pay higher prices.

An example of cost-push inflation

As of April 2022, Australia’s unemployment rate is a very low 4 per cent. This means that businesses may find it hard to secure workers as many people are already employed. To attract workers, firms may need to pay higher wages. And wages are a cost for businesses.

A firm could absorb the higher wages cost. But this would reduce their profit (as profit = revenue - costs). Instead, the firm will pass on the cost of higher wages to consumers in the form of higher prices. Consumers will ultimately pay for the higher employee wages.

When prices rise, inflation rises. In our example, input costs (wages) have pushed inflation higher.

Other sources of cost-push inflation could be higher energy prices (electricity or petrol), more expensive food and higher rental costs.

How cost-push inflation works

Cost-push inflation in the Australian economy in 2022

National Australia Bank (NAB), one of Australia’s big four banks, publishes a monthly business survey. According to the survey, firms’ purchase costs (the cost of their inputs) rose by 4.2 per cent in the March quarter.

[The March quarter covers January, February and March.]

This 4.2 per cent rise is a record for the NAB survey. The survey also found that labour costs — as discussed in our example above — rose by 2.7 per cent in the March quarter. This was another record rise.

NAB Chief Economist Alan Oster said that many industries were experiencing rising input costs. This is what the survey calls ‘purchase costs’.

“Purchase costs reached records with elevated oil prices adding to existing supply chain issues, and labour costs are also rising as businesses hire more workers in a very competitive labour market,” Mr Oster said.

These rising input costs are leading directly to higher prices. According to the NAB survey, retail prices rose by 3.7 per cent over the March quarter of 2022. This is a record level for the survey.

Why does cost-push inflation matter?

Rising cost-push inflation is another sign that Australia’s inflation rate is rising (potentially rapidly) . This adds to the likelihood that the Reserve Bank of Australia will soon begin raising the cash rate to try and control inflation. The RBA meets monthly and many economists believe the cash rate could be raised as soon as June 2022.

When we talk about the RBA raising rates, we’re discussing monetary policy. Check out this article for more about this important macroeconomic policy.

5 observations on the 2021-22 Federal Budget

The 2021-22 Federal Budget was handed down on 11 May 2021. Here are my five quick observations.

1. The Federal Budget is HIGHLY expansionary

Yes, the size of the budget deficit is shrinking. This means that the budget stance, technically, is contractionary between 2021-22 and 2024-25.

For instance, in 2021-22, the budget deficit is forecast to be $106.6 billion. In 2024-25, it’s forecast to be $57 billion.

But, don’t get it twisted. The budget is still in deficit. The government is still planning to spend substantially more than it earns in revenue (mainly tax revenue). Therefore, the overall impact of Fiscal Policy is expansionary...even if the stance is contractionary between the years.

2. The Federal Budget is about more than stimulating aggregate demand

A major part of the budget involves a large increase in spending on the aged care sector. This is in response to the Royal Commission into aged care which found deficiencies in a number of areas.

This is increased government spending, but it’s not about boosting AD or increasing productivity. After all, this spending is going towards older Australians who are in nursing homes or receiving full-time care at home.

Instead, this measure is largely about improving the quality of life of older Australians. This is an important goal of the government, but it’s more social than economic.

3. The Federal Budget’s boost on childcare spending is an economic measure

The government is offering larger childcare subsidies for parents. The goal here is economic; the goal here is twofold.

One, give people more disposable income by reducing the costs of childcare. (FYI: childcare is very expensive). Parents will spend less on childcare, spend more on consumption...and this will in turn boost AD.

Two, by making childcare cheaper the government is encouraging more parents to use it. The government is actually increasing demand for childcare. This means more parents will be able to work more hours, or potentially return to the labour force. According to Treasury, this will boost the number of hours worked in the Australian economy by 300,000 hours.

4. Fiscal Policy and Monetary Policy are working in tandem

In the past, FP and MP have worked in opposing directions. The RBA had cut the cash rate extensively, however the Morrison Government was keen to protect its goal of a budget surplus and so did not adopt an expansionary stance.

Now both MP and FP are highly expansionary. By working together, it’s hoped their impact on stimulating aggregate demand will be enhanced.

Also, some economists have discussed that the very low cash rate — 0.1% since November 2020 — means that future cuts would not have a major economic impact. If the RBA cuts from 0.1% to 0%, would that dramatically increase consumption and investment? Just remember, the cash rate might be zero but interest rates would not be. The banks would still be looking for a profit margin.

Instead, FP is helping to take up some of the slack.

5. The Federal Government has committed to a return to fiscal discipline

Fiscal discipline or fiscal consolidation is all about moving from a budget deficit back to balanced or surplus budget outcome. The Morrison Government has told us that, yes, we’re in large deficits and, yes, this will persist for some time...but the size of the deficit will be shrinking and there is a target for a return to less expansionary fiscal policy.

The target? When unemployment falls below 5%.

Overall thoughts

In terms of a ‘conclusion’, I really like this article by economist Steven Hamilton. His point of view is that budget deficits are necessary, for now, to drag Australia along the road to recovery. But they cannot persist forever and the government has committed to turn off the expansionary setting once UE falls below its target.

Tough times for the Australian economy, says RBA

Four times a year, the Reserve Bank of Australia (RBA) shares its assessment of current economic conditions for Australia and the world. This document is called the Statement of Monetary Policy (SOMP). The SOMP for May 2020 sets out some serious challenges for the Australian economy.

I think, as a student, the most important section to focus on is Section 6: Economic Outlook.

I discussed this section in a previous post that looked at the RBA’s three potential scenarios involving the Australian economy’s recovery from COVID-19.

In this post, I’ll take a look at some specific economic forecasts from its May SOMP.

Economic growth

According to the RBA, the Australian economy is “expected to record a contraction in GDP of around 10 per cent over the first half of 2020”. Considering Australia’s GDP grew by around 4 per cent in the first half of 2019, this is a huge turnaround — in a negative sense.

Why is GDP expected to plummet? Well, social distancing means people aren’t going to the shops and spending. The RBA forecasts household spending to fall by 15 per cent in the June quarter this year. In addition, consumers are saving more, as people tend to do in times of uncertainty.

Australia is also not receiving international visitors and their tourist spending. This is classified as export revenue for Australia, and a component of aggregate demand (AD). Less exports mean less economic growth for Australia.

On the flip side, Australians are expected to spend much less on imports.

Unemployment

The RBA estimates that total hours worked in the Australian economy will fall by around 20 per cent in the June quarter (the three months to June 2020). In addition, the RBA says unemployment could rise to around 10 per cent by the same point in time.

Considering the unemployment rate was 5.2 per cent in March 2020, this could represent a near doubling of the number of Australians out of work.

But here’s the thing: while the unemployment rate may not increase by this much, we should still be concerned.

This is because of what’s called “the discouraged worker effect”. This is when an individual gives up looking for work because they don’t believe they will be able to get a job. If people give up looking for work, they’re not considered unemployed and they’d join the hidden unemployed.

(In Australia, to be considered unemployed, you must be out of work and actively seeking a job.)

So Australia’s unemployment rate may not increase by the expected amount, but the economy would still have lost substantial labour resources.

Inflation

Australia, for some time pre-COVID-19, has recorded relatively low inflation rates. This has been part of the reason why the RBA had steadily cut official interest rates.

Due to the pandemic, the RBA expects inflation to turn negative in the June quarter. So: Australia would record deflation.

Why would this happen? Two main reasons. One, fuel prices have fallen dramatically. Just have a look at this chart of unleaded petrol prices in Sydney and how they’ve fallen this year.

Source: PetrolSpy

Two, the Federal Government is providing free childcare to families. So the price of childcare has fallen from something to, well, nothing. These two factors will drag down headline inflation.

The Australian economy in 2020 (maybe)

What should we expect from the Australian economy in 2020?

Forecasting the future is a tough game, but economist Stephen Koukoulas has given it a go. In an article for Yahoo Finance, Koukoulas has taken a look ahead into the future for the Australian economy. I’ve focused on four of his predictions and you can read his full article for more.

Australia’s Economic Growth

In 2019, Australia’s annual growth in gross domestic product (GDP) was relatively weak. GDP averaged around 1.7 per cent in annual terms. Compare that with the government’s goal for economic growth of around 3-4 per cent in annual terms.

In his article, Koukoulas presents an optimistic case for Australia’s GDP. He suggests it could reach 2.5 per cent by mid-2020 and perhaps as high as 3 per cent by the end of this year.

His relative optimism is based on three factors:

A rise in public sector spending, particularly in infrastructure (this represents government spending, or G, in the aggregate demand equation)

Increased business investment, potentially helped by record low interest rates in Australia

Increased consumption, boosted by a recovery in consumer confidence and the wealth effect (where rising asset prices, house prices in Australia’s case, encourage consumers to boost spending).

Australia’s Unemployment

In 2019, Australia’s labour market was relatively weak and unemployment did not budge far from the 5 to 5.2 per cent range. Koukoulas believes UE could rise even further to around 5.5 per cent in 2020.

But! If the predictions around higher economic growth come true, unemployment will likely fall. Koukoulas states that if GDP growth hits 3 per cent, then we will see noticeable falls in unemployment and underemployment.

Why is this the case? Well, if economic growth rises, this means there is greater production of goods and services in the Australian economy. To achieve this, local firms will need additional factors of production (or resources) — particularly labour. They will demand more labour, which will push down UE. (This is known as derived demand, where the demand for labour is derived from the demand for goods and services).

Inflation in Australia

The Reserve Bank of Australia’s goal is to keep inflation between 2 to 3 per cent over the course of the business cycle. This is known as the target band. For the duration of 2019, Australia’s inflation rate was below the target band.

Koukoulas says if the economic growth mentioned above takes place, inflation will likely rise to 2 per cent or to sit inside the target band. This demonstrates the link between economic growth and inflation: as economic growth rises, the demand for goods and services will also rise, leading to higher prices and inflation.

The Australian Dollar

In late 2019, the $A traded around the US$0.66-US$0.68 mark. However, Koukoulas believes the $A could be trading as high as US$0.77 in 2020.

He presents two potential reasons for this appreciation:

Improving global economic growth will lead to higher demand for Australia’s commodity exports. This will increase demand for the $A as buyers need local currency to purchase Australian exports.

Improving domestic conditions could lead to greater investment in the Australian economy. To participate in this, foreign investors will need $A, which will also cause the currency to appreciate.

One point I would add here is that a stronger $A will make exports more expensive and less internationally competitive. This could result in Australia actually selling fewer exports, which may have negative consequences for the trade balance and the Balance of Payments.

We’ll be watching this year to see how these forecasts unfold.

Making aggregate demand simple(r)

Aggregate demand (and supply) can be relatively complex concepts for students.

I was teaching AD one day and thought about how when we talk about aggregate, we’re focusing on total. So if think about AD we’re thinking about every individual demand curve in an economy added together.

In terms of demand curves, it’s the sum of Dean’s and Daniel’s and Hannah’s and mine and yours and...you get the picture.

This description might help students clarify their understanding. Check out the video below too.