Four graphs that explain the 2022 Federal Budget

QUICK SUMMARY

The 2022-23 Federal Budget was handed down in March 2022

The Morrison Government is forecasting ongoing budget deficits (government spending exceeds government revenue)

However, the Morrison Government forecasts that the size of the budget deficits will shrink over the next decade

The most important factor: the reduction in government spending and increase in tax revenue as the economy improves during the COVID-19 pandemic.

In this blog post, I’ll look at these four graphs (click the links to jump there):

Total government payments (spending) and receipts (revenue)

Size of Australian government debt

Australia’s government debt levels compared to other advanced economies

Graph one: The budget balance

This graph (labelled Chart 3.2 below) shows how the budget deficit will shrink to approach a balanced budget by 2032-33.

Overall, this graph shows the size of the budget balance as a percentage of GDP. If the number is positive, Australia has a budget surplus. If the number is negative, Australia has a budget deficit. If the number is zero — the budget is balanced.

Look at the black line. Before COVID, the federal budget was balanced and potentially returning to surplus. Once the pandemic hits, the government significantly increases spending to help ease the effects of COVID. As a result, the black line plummets and Australia’s budget deficit peaks at around 6 per cent of GDP (the -6% number).

Then follow the blue line. This is the Morrison Government’s forecasts for how the budget balance will change. The point: the government expects the budget deficit to shrink.

In economic terms, this is known as “fiscal consolidation” or “fiscal repair”, where the government is running contractionary fiscal policy to reduce the budget deficit and return to a balanced or surplus budget.

So the government is forecasting an ongoing improvement in the budget balance to approach a balanced budget in 2032-33. Note: the further out the forecasts, the less certain we can be about them.

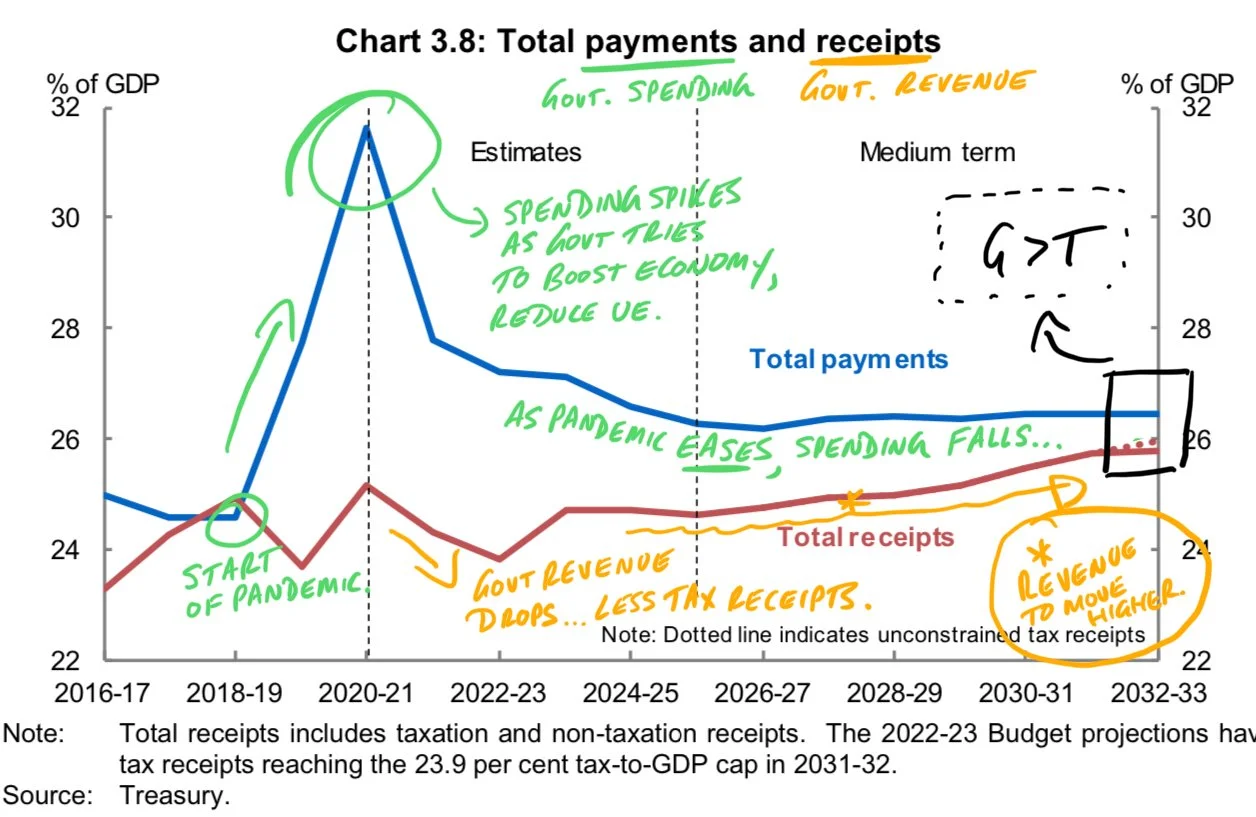

Graph two: Total government payments (spending) and receipts (revenue)

This graph (labelled Chart 3.8 below) shows that Government spending spiked during 2021 and is substantially falling as the temporary COVID-related spending decreases or ends.

The red line is government revenue, which mainly comes from individual and company tax. The blue line is government spending, which is dominated by spending on welfare payments.

Focus on the left hand side of the graph. You can see that the blue and red lines intersect. This shows us that spending was equal to revenue and the budget was balanced.

As the pandemic starts, government spending significantly increases. You can see that government spending peaks at around 32 per cent of GDP as the Morrison Government tried to offset the worst impacts of COVID. This included significant spending on Job Seeker and Job Keeper programs that aimed to keep people employed, even as businesses had to temporarily close or restrict trading, and stop unemployment rapidly rising.

At the same time, revenue decreased at certain points — but not as significantly. This was due to lower tax revenue as more people were unemployed and companies earned lower profits (because they were forced to shut during lockdowns).

Take a look at the period from 2022-23 onwards. Pandemic-related spending is projected to substantially fall. At the same time, as the Australian economy is forecast to recover and grow more rapidly, government revenue is projected to increase. This will shrink the difference between government spending and government revenue.

This, in turn, will shrink the size of the budget deficit.

So the reason why the government is forecasting smaller budget deficits is because:

Less spending on programs that were designed to protect the economy from the effects of COVID

More revenue as the Australian economy recovers from COVID.

This is evident from the graph — the shrinking distance between the blue and red lines.

Graph three: Size of Australian Government debt

According to the 2022 Federal Budget, the Morrison Government forecasts that the size of federal government debt will shrink more quickly than previously thought.

This chart (labelled Chart 3.1 below) shows the size of the federal government’s debt.

A quick note about debt and deficit. The budget deficit means that there is a discrepancy between government spending and revenue. Government spending exceeds government revenue. This creates a deficit of funds in the federal budget because the government is spending more than it earns.

And if the government has a deficit, it needs to find the funds to pay for its extra spending. To fund the gap between spending and revenue, the government will borrow money from overseas. That is, it will incur more debt.

Have a look at the left hand side of the graph. Pre-pandemic, the government’s debt was relatively flat around 30 per cent of GDP. COVID hits, the Morrison Government starts spending to try and protect the Australian economy and stop unemployment soaring. To pay for this extra spending, the government borrowed increasing amounts of money from overseas.

The three lines show us that, over the past three years, the government has forecast that the amount of funds it needs to be borrow will be less and less. For example, in the 2020-21 budget, the Morrison Government forecast that government debt might get to around 55 per cent of GDP. However, as the Australian economy has improved and the budget deficit is projected to shrink, the amount of debt is also expected to shrink. Now, the government expects debt will fall to around 40 per cent of GDP by 2032-33.

Here’s the key thing: as the budget deficit shrinks, the government will need to borrow less money to fund the gap between spending and revenue. This means the size of government debt will also fall.

Graph four: Australia’s government debt compared to other advanced economies

The Australian Government’s debt (as seen in Chart 3.9 below) can be considered comparable or low compared to other developed economies.

The graph above shows how all G7 economies have increased spending and their debt levels because of COVID. However, this graph shows that the size of Australia’s debt levels is either similar to or substantially lower than the debt levels of G7 economies.

For example, in the US, government debt levels exceed 100 per cent of GDP. And these levels are even higher in Italy and Japan.

The important thing to think about is that the larger the amount of debt, the longer it will take to repay and the greater amount of interest payments required to service these loans. This could be an issue as global interest rates are expected to rise over 2022.

One last thing

Here’s a small summary table from the 2022 Federal Budget that shows how the Morrison Government expects the budget deficit to shrink over the next five years. These numbers are great to have handy for essay questions on fiscal policy.

And here’s a short explainer on how changes in the federal budget then affect the Australian economy.

5 observations on the 2021-22 Federal Budget

The 2021-22 Federal Budget was handed down on 11 May 2021. Here are my five quick observations.

1. The Federal Budget is HIGHLY expansionary

Yes, the size of the budget deficit is shrinking. This means that the budget stance, technically, is contractionary between 2021-22 and 2024-25.

For instance, in 2021-22, the budget deficit is forecast to be $106.6 billion. In 2024-25, it’s forecast to be $57 billion.

But, don’t get it twisted. The budget is still in deficit. The government is still planning to spend substantially more than it earns in revenue (mainly tax revenue). Therefore, the overall impact of Fiscal Policy is expansionary...even if the stance is contractionary between the years.

2. The Federal Budget is about more than stimulating aggregate demand

A major part of the budget involves a large increase in spending on the aged care sector. This is in response to the Royal Commission into aged care which found deficiencies in a number of areas.

This is increased government spending, but it’s not about boosting AD or increasing productivity. After all, this spending is going towards older Australians who are in nursing homes or receiving full-time care at home.

Instead, this measure is largely about improving the quality of life of older Australians. This is an important goal of the government, but it’s more social than economic.

3. The Federal Budget’s boost on childcare spending is an economic measure

The government is offering larger childcare subsidies for parents. The goal here is economic; the goal here is twofold.

One, give people more disposable income by reducing the costs of childcare. (FYI: childcare is very expensive). Parents will spend less on childcare, spend more on consumption...and this will in turn boost AD.

Two, by making childcare cheaper the government is encouraging more parents to use it. The government is actually increasing demand for childcare. This means more parents will be able to work more hours, or potentially return to the labour force. According to Treasury, this will boost the number of hours worked in the Australian economy by 300,000 hours.

4. Fiscal Policy and Monetary Policy are working in tandem

In the past, FP and MP have worked in opposing directions. The RBA had cut the cash rate extensively, however the Morrison Government was keen to protect its goal of a budget surplus and so did not adopt an expansionary stance.

Now both MP and FP are highly expansionary. By working together, it’s hoped their impact on stimulating aggregate demand will be enhanced.

Also, some economists have discussed that the very low cash rate — 0.1% since November 2020 — means that future cuts would not have a major economic impact. If the RBA cuts from 0.1% to 0%, would that dramatically increase consumption and investment? Just remember, the cash rate might be zero but interest rates would not be. The banks would still be looking for a profit margin.

Instead, FP is helping to take up some of the slack.

5. The Federal Government has committed to a return to fiscal discipline

Fiscal discipline or fiscal consolidation is all about moving from a budget deficit back to balanced or surplus budget outcome. The Morrison Government has told us that, yes, we’re in large deficits and, yes, this will persist for some time...but the size of the deficit will be shrinking and there is a target for a return to less expansionary fiscal policy.

The target? When unemployment falls below 5%.

Overall thoughts

In terms of a ‘conclusion’, I really like this article by economist Steven Hamilton. His point of view is that budget deficits are necessary, for now, to drag Australia along the road to recovery. But they cannot persist forever and the government has committed to turn off the expansionary setting once UE falls below its target.

Um, discretionary and non-discretionary fiscal policy, much?

Let’s turn our attention to fiscal policy. Fiscal policy is budget policy, it’s how the government adjusts government spending and revenue to meet economic objectives. The government might be trying to rev up the economy or achieve a surplus. And within fiscal policy, there are things the government can and can’t control.

Let me explain.

Fiscal policy consists of discretionary and non-discretionary factors. Discretionary signals ‘discretion’, as in choice. Will you get in trouble? It’s up to the discretion of your teacher.

When it comes to the budget, discretionary factors (also known as structural factors) are the deliberate choices a government makes. This could include expenditure measures like building a new hospital or buying a new fleet of tanks for the Defence Force. On the revenue side, the government could make a deliberate choice to cut tax rates.

It all depends on what the government wants to achieve.

But the budget also contains non-discretionary (or cyclical) factors. These are the factors that are not controlled by government, also known as automatic stabilisers. These factors, such as unemployment benefits and taxation revenue, depend on the level of economic activity. They work in a counter-cyclical way, without the government doing anything.

For example, in boom times, unemployment benefits will fall and tax revenue will increase, thus slowing down the economy. This happens without the government doing anything!

“Fiscal policy has its own brain. (Not like an actual brain, like a metaphorical brain.)”

I put it like this to my students: fiscal policy (non-discretionary fiscal policy) has its own brain. It decides what to do, without even consulting the government. It just operates automatically.

So just to recap:

Non-discretionary (cyclical) factors are not controlled by the government. They depend on the level of economic activity. Examples include unemployment benefits and taxation revenue (see ‘quick note’ below)

Discretionary (structural) factors are deliberate decisions made by government.

A quick note

If the government cuts tax rates, this is a discretionary choice. The government sets the tax brackets and can seek to change them as it sees fit.

The government cannot control the amount of tax revenue collected. This is non-discretionary. This is because, while the government can set tax rates, it cannot control the level of people’s income. So the overall amount of tax revenue collected is a cyclical factor.

What if tax cuts don’t get people spending?

Economic theory states: tax cuts are stimulatory. They will boost aggregate demand and support economic growth. But what if they don’t?

Let’s rewind a step. In terms of people’s incomes, there are three things that happen with their money. They can spend their money, they can save it and they have to pay tax. Sigh. This relationship is neatly summarised by:

Y=C+S+T

(Where Y is income, C is consumption, S is saving and T is tax.)

After Saturday’s election in Australia, the Morrison Government has been re-elected and it’s now figuring out how to implement its proposed tax cuts. Under the tax cuts, people earning up to $126,000 will get $1,080 back at tax time. This potential economic stimulus is so large that it could be equivalent to TWO Reserve Bank of Australia rate cuts, each of 25 basis points (according to the Commonwealth Bank of Australia’s economics team).

"The RBA [may] refrain from taking the cash rate lower because they know that household consumption will pick up in the second half of 2019 courtesy of the tax relief,” says CBA senior economist Gareth Aird.

But what if consumer don’t spend their extra income? What if they save?

In recent years, the size of the average Australian mortgage has been rising (mortgage payments now make up 34% of household incomes). At the same time, Australia has relatively low household savings rates (see graph below). If households are given a bunch of extra money, they could save it, depending on their marginal propensity to save or spend.

The marginal propensity to save (MPS) or spend (MPC, C for consumption) is what proportion of every extra dollar in income will be spent or saved.

Australia’s household savings ratio — peep that decline!

My point here is that, as economists, we need to factor in the possibility that the government’s policies may not have their intended impact. Or they may not have as large an impact as the government would like.

How can you use this information?

When you’re talking about fiscal policy for 2019-20, mention the Morrison Government’s tax cuts and their impact according to economic theory. But also include the possibility that households will save, not spend.

Mention the potential impact of these tax cuts: equivalent to an RBA rate cut of 25 basis points. So, very stimulatory.

The difference between fiscal and monetary policy

It can be tricky to distinguish between fiscal and monetary policy.

Let’s try and make it a bit easier.

Fiscal policy is all about the federal government’s use of the federal budget. It’s about the government changing government spending (an injection, the symbol is G) and taxation revenue (a leakage, the symbol is T) to affect the level of economic activity…and achieve other economic objectives.

Fiscal policy is budget policy.

Monetary policy is different.

Monetary policy involves the Reserve Bank of Australia’s (RBA) actions to alter the value of the cash rate to control the level of inflation (and affect economic growth). The RBA changes the cash rate to create changes in the general level of interest rates (set by the commercial banks) to deal with inflation and growth and employment and other challenges.

Big thing to note: monetary policy is government policy. But the government does not implement monetary policy.

Monetary policy is implemented by the independent RBA, on behalf of the government.

Fiscal policy: think about the budget.

Monetary policy: think about interest rates and the RBA.

Hope this helps. Try this video too.

Understanding automatic stabilisers

This is a tough one. But, rather than explain it to you with words, I’m going to explain it to you with pictures.

This video about automatic stabilisers is one of the first Eco videos I created. Audio’s not great, but stay tuned for the hilarity.

Once you’ve seen the videos, answer the questions in the sheets. Super helpful for consolidating your knowledge about this weird concept.

Questions in the comments pls.

Why are Australia’s macroeconomic policies fighting?

At 2:30pm today, the Reserve Bank of Australia kept the cash rate on hold at 1.5 per cent. Economists weren’t sure what the RBA would do: would it cut rates further? Would it keep them steady? . So the decision surprised some. But this isn’t the most interesting thing.

What I find most interesting is the conflict between Australia’s macroeconomic policies.

[See my instant reaction video about the RBA’s decision.]

As a quick refresher, macroeconomic policies are policies that affect the whole economy, not just one sector. The major macro policies are monetary policy (the RBA’s influencing the general level of interest rates in the economy) and fiscal policy (the use of the Federal Budget).

These macro policies can be used to speed up or slow down the economy. In terms of achieving goals, it’s helpful if they’re working in the same direction and not against each other.

But check this out. Monetary policy is wildly expansionary. It is at historic lows, in an attempt to increase Australia’s pretty average economic growth rates. At the same time, fiscal policy is contractionary. That is, the government is trying to create a budget surplus (a situation where government revenue, a leakage, exceeds government spending, an injection).

Put simply: monetary policy is trying to expand the economy, fiscal policy is actually working to slow it down.

Why are they working in opposite directions? Part of it is the federal government’s attempts to quickly return the nation’s budget back to surplus. The RBA is independent of government, so it’s pursuing a different plan.

It gets even more complicated, though. The federal government is planning to run a budget surplus...but it is planning to implement major tax cuts (an injection) if it wins the upcoming election. So, even within fiscal policy, the government is trying to achieve competing goals.

AS A STUDENT, HOW CAN I USE THIS INFORMATION?

When you’re writing about Australia’s use of macroeconomic policies, discuss the conflicts between the policies themselves

You can also discuss conflicts WITHIN fiscal policy, where different measures are working to slow and expand the economy simultaneously

Make sure to mention that fiscal policy is controlled by the federal government, while the independent RBA handles monetary policy